Home Equity Line of Credit (HELOC) in California

California homeowners have built significant equity over the past several years — and a Home Equity Line of Credit (HELOC) is one of the smartest ways to put that equity to work. Whether you want to renovate your home, consolidate high-interest debt, fund a business, cover college costs, or purchase an investment property, a HELOC gives you flexible access to the cash you need at a far lower rate than credit cards or personal loans.

At Billcutter, we specialize in California HELOC loans with fast approvals, competitive rates, and a streamlined process. We can often close a HELOC in days — not weeks.

What Is a HELOC?

A Home Equity Line of Credit is a revolving line of credit secured by your home. Unlike a traditional loan where you receive a lump sum, a HELOC works more like a credit card — you're approved for a credit limit, and you draw only what you need, when you need it.

How it works:

- Draw Period (typically 10 years): You can borrow up to your credit limit, repay, and borrow again. Payments are usually interest-only during this period.

- Repayment Period (typically 10-20 years): The line closes and you repay the outstanding balance in full, usually with principal + interest payments.

How Much Can You Borrow?

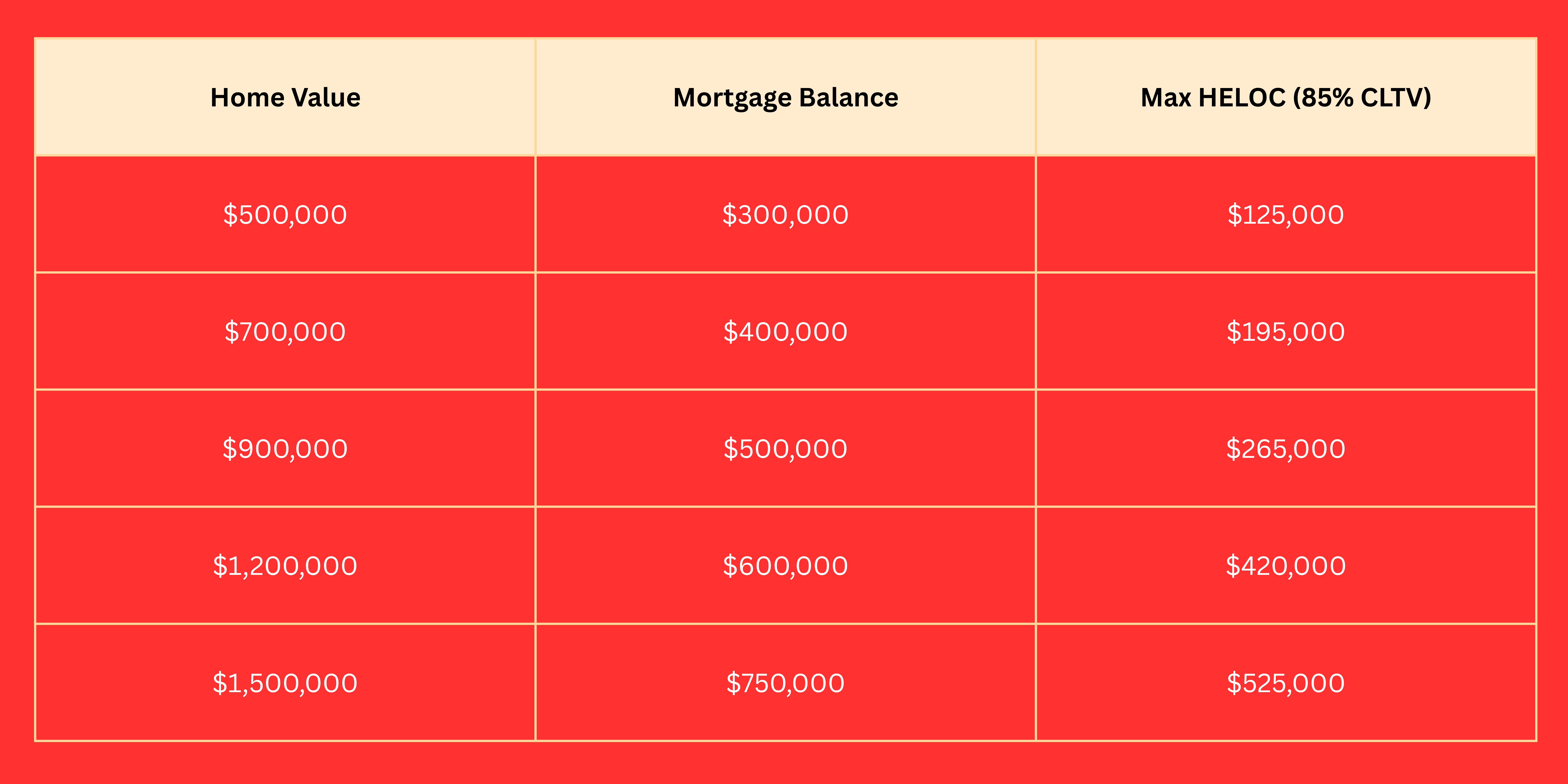

Your HELOC limit is based on your home's value and how much you owe on your mortgage.

The formula:

(Home Value × 85%) − Current Mortgage Balance = Maximum HELOC Amount

Example:

- Home value: $700,000

- Current mortgage balance: $400,000

- Maximum HELOC: ($700,000 × 85%) − $400,000 = $195,000

With California's strong home values, many homeowners qualify for HELOCs of $100,000 to $500,000+.

Billcutter HELOC Program Details

- Loan amounts: $20,000 to $500,000+

- Max LTV: Up to 85% combined loan-to-value

- Draw period: 10 years

- Repayment period: Up to 20 years

- Rate type: Variable rate tied to Prime Rate

- Closing time: Often 5-15 business days

- Won't affect your first mortgage rate

- Available throughout California

What Can You Use a HELOC For?

A HELOC is one of the most flexible financial tools available. California homeowners use HELOCs for:

Home Improvements & Renovations

The most common use — and one of the smartest. Reinvesting equity into your home increases its value, often returning more than you spent.

Popular projects: kitchen remodel, bathroom remodel, ADU construction, solar installation, room addition, landscaping

Debt Consolidation

Credit card debt at 20-25% APR costs you significantly more than a HELOC at 7-10% APR. Many Californians use a HELOC to pay off high-interest debt and reduce their monthly obligations dramatically.

Real Estate Investment

Use your primary home's equity to fund a down payment on an investment property or vacation home — essentially using your equity to buy more equity.

Business Investment

Self-employed business owners often use HELOCs as flexible working capital or to fund business growth without taking on business debt.

Education Expenses

College tuition, private school, or professional certifications — HELOC rates are far lower than student loans in most cases.

Emergency Fund

Having an open HELOC (even if you don't draw on it) provides a powerful safety net for unexpected expenses without paying interest until you actually use it.

HELOC Requirements in California

Typical qualification guidelines:

- Credit score: 620+ (700+ for best rates)

- Combined LTV: Up to 85%

- Debt-to-income ratio: Generally under 43-50%

- Home equity: At least 15-20% equity required

- Property types: Primary residence, second home, investment property (varies by lender)

- Documentation: Income verification, property appraisal or AVM

Self-employed borrowers: Billcutter also offers Non-QM HELOC options for borrowers who can't qualify using traditional income documentation. Bank statement qualification available.

HELOC Rates in California

HELOC rates are variable and tied to the Prime Rate, which moves with Federal Reserve decisions. As of 2026, HELOC rates in California typically range from 7.5% to 10.5% depending on:

- Your credit score

- Combined loan-to-value ratio

- Lender and program

- Draw amount

Rates are significantly lower than credit cards (18-25%), personal loans (10-20%), and most other unsecured debt.

Contact Billcutter for a personalized rate quote — rates vary by borrower and change frequently.

Why Choose Billcutter for Your HELOC?

Fast Closings

We close HELOCs faster than traditional banks — often in 5-15 business days. When you need access to funds, waiting months isn't an option.

Broker Access to Multiple Lenders

We work with dozens of wholesale lenders, meaning we can find the most competitive HELOC rate available for your situation — not just what one bank offers.

Specialists for Complex Situations

Self-employed? Recent credit event? Non-warrantable condo? We have solutions where traditional lenders say no.

California Expertise

We understand California real estate values, property types, and the unique needs of California homeowners.

No Obligation Consultation

We'll review your situation, tell you exactly what you qualify for, and give you a rate quote — at no cost and no commitment.

Frequently Asked Questions

How quickly can I get a HELOC?

Billcutter can often close a HELOC in 5-15 business days — significantly faster than most banks. The timeline depends on appraisal turnaround and your documentation.

Will a HELOC affect my first mortgage?

No. A HELOC is a second lien on your property. Your first mortgage rate, payment, and terms remain completely unchanged.

Is HELOC interest tax deductible?

HELOC interest may be tax deductible if the funds are used to buy, build, or substantially improve your home. Consult a tax professional for guidance specific to your situation.

Can I get a HELOC on an investment property?

Yes — some lenders offer HELOCs on investment properties, typically at slightly higher rates and lower LTV limits. Contact us to discuss your specific property.

What happens if home values drop?

Lenders can freeze or reduce your HELOC if your home value drops significantly (as happened in 2008-2009). This is worth considering if you're in a market with elevated risk.

Can I get a HELOC if I'm self-employed?

Yes — Billcutter offers bank statement and Non-QM HELOC options for self-employed borrowers who can't qualify using traditional income documentation.

What's the difference between a HELOC and a HELOAN?

A HELOC is a revolving credit line (variable rate, draw as needed). A HELOAN (Home Equity Loan) is a fixed-rate lump sum. A HELOC offers more flexibility; a HELOAN offers payment certainty. We offer both.

Serving HELOC Borrowers Across California

Billcutter offers HELOCs throughout California including:

- HELOC in Los Angeles

- HELOC in Orange County

- HELOC in San Diego

- HELOC in the Inland Empire — Riverside and San Bernardino Counties

- HELOC in the Bay Area

Ready to Unlock Your Home's Equity?

Find out how much you can access in minutes — no credit check, no commitment.

Our team is ready to help you make the most of the equity you've worked hard to build.

Call a Loan Officer at (888) 855-1423 or apply online.